All Categories

Featured

Table of Contents

Section 691(c)( 1) offers that a person that includes an amount of IRD in gross revenue under 691(a) is enabled as a deduction, for the very same taxable year, a portion of the inheritance tax paid because the addition of that IRD in the decedent's gross estate. Generally, the quantity of the deduction is computed using inheritance tax worths, and is the quantity that bears the same proportion to the estate tax obligation attributable to the web value of all IRD items consisted of in the decedent's gross estate as the worth of the IRD included in that person's gross earnings for that taxed year births to the worth of all IRD items consisted of in the decedent's gross estate.

Section 1014(c) provides that 1014 does not apply to home that constitutes a right to obtain a thing of IRD under 691. Rev. Rul. 79-335, 1979-2 C.B. 292, attends to a circumstance in which the owner-annuitant purchases a deferred variable annuity agreement that gives that if the proprietor passes away before the annuity beginning date, the called recipient may choose to obtain the here and now collected worth of the agreement either in the type of an annuity or a lump-sum payment.

Rul. 79-335 ends that, for objectives of 1014, the agreement is an annuity explained in 72 (as after that basically), and as a result obtains no basis modification because the proprietor's fatality because it is controlled by the annuity exception of 1014(b)( 9 )(A). If the beneficiary chooses a lump-sum settlement, the extra of the amount got over the quantity of consideration paid by the decedent is includable in the recipient's gross earnings.

Rul (Guaranteed annuities). 79-335 concludes that the annuity exemption in 1014(b)( 9 )(A) puts on the agreement described because judgment, it does not specifically attend to whether amounts obtained by a beneficiary under a postponed annuity agreement over of the owner-annuitant's investment in the agreement would go through 691 and 1014(c). Had the owner-annuitant gave up the contract and obtained the amounts in extra of the owner-annuitant's financial investment in the contract, those amounts would certainly have been earnings to the owner-annuitant under 72(e).

Inheritance taxes on Annuity Income

Similarly, in today situation, had A surrendered the contract and obtained the amounts at concern, those amounts would have been revenue to A under 72(e) to the degree they surpassed A's investment in the contract. Appropriately, amounts that B receives that surpass A's financial investment in the contract are IRD under 691(a).

Rul. 79-335, those amounts are includible in B's gross earnings and B does not receive a basis adjustment in the contract. B will be entitled to a deduction under 691(c) if estate tax obligation was due by reason of A's fatality. The outcome would coincide whether B obtains the survivor benefit in a lump sum or as periodic payments.

DRAFTING Info The principal author of this earnings ruling is Bradford R.

Joint And Survivor Annuities inheritance tax rules

Q. How are just how taxed as strained inheritance? Is there a difference if I inherit it directly or if it goes to a depend on for which I'm the beneficiary? This is a fantastic inquiry, yet it's the kind you need to take to an estate planning attorney who understands the details of your circumstance.

For instance, what is the connection between the dead owner of the annuity and you, the recipient? What sort of annuity is this? Are you asking about income, estate or inheritance tax obligations? Then we have your curveball question concerning whether the result is any kind of various if the inheritance is with a trust or outright.

We'll assume the annuity is a non-qualified annuity, which implies it's not component of an IRA or various other certified retirement plan. Botwinick said this annuity would be added to the taxed estate for New Jacket and federal estate tax purposes at its day of death worth.

Taxation of inherited Annuity Cash Value

resident partner exceeds $2 million. This is called the exemption.Any amount passing to an U.S. person partner will be totally excluded from New Jersey estate tax obligations, and if the owner of the annuity lives to the end of 2017, then there will certainly be no New Jersey estate tax on any amount because the estate tax is set up for repeal beginning on Jan. After that there are government inheritance tax.

The present exception is $5.49 million, and Botwinick stated this tax is possibly not disappearing in 2018 unless there is some significant tax obligation reform in an actual rush. Like New Jacket, government inheritance tax legislation gives a full exemption to quantities passing to making it through U.S. Next, New Jacket's inheritance tax.Though the New Jersey estate tax obligation is scheduled

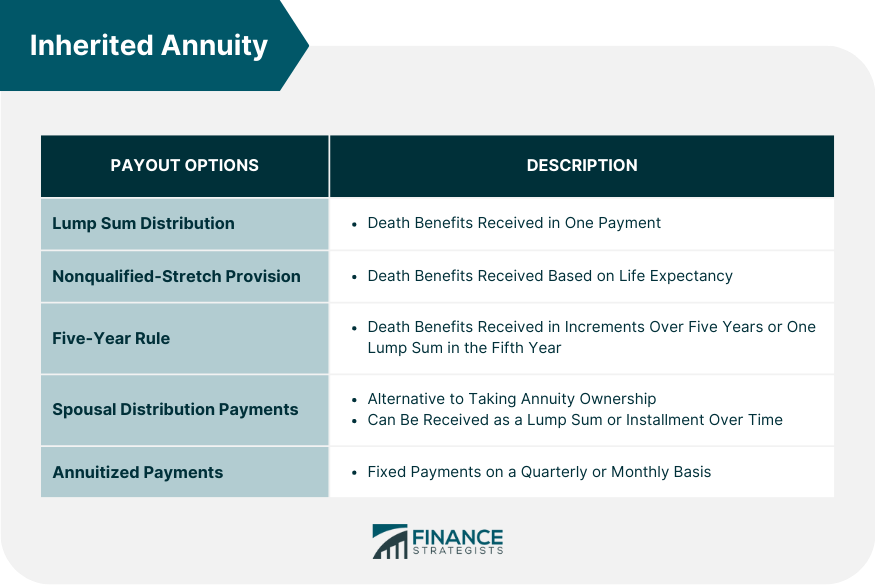

to be repealed in 2018, there is noabolition scheduled for the New Jersey estate tax, Botwinick said. There is no federal inheritance tax. The state tax gets on transfers to everybody apart from a specific class of individuals, he said. These consist of partners, youngsters, grandchildren, moms and dad and step-children." The New Jacket estate tax applies to annuities simply as it applies to various other properties,"he claimed."Though life insurance payable to a specific beneficiary is exempt from New Jersey's inheritance tax, the exception does not relate to annuities. "Currently, income taxes.Again, we're thinking this annuity is a non-qualified annuity." Essentially, the proceeds are taxed as they are paid. A section of the payment will certainly be dealt with as a nontaxable return of investment, and the profits will be strained as normal revenue."Unlike acquiring various other properties, Botwinick stated, there is no stepped-up basis for acquired annuities. Nonetheless, if estate tax obligations are paid as an outcome of the inclusion of the annuity in the taxable estate, the recipient might be qualified to a reduction for inherited income in regard of a decedent, he said. Annuity repayments include a return of principalthe cash the annuitant pays right into the contractand passionmade inside the contract. The rate of interest section is taxed as normal income, while the principal quantity is not taxed. For annuities paying over an extra extensive duration or life expectations, the principal part is smaller, leading to fewer tax obligations on the month-to-month settlements. For a wedded pair, the annuity agreement might be structured as joint and survivor to ensure that, if one spouse dies , the survivor will proceed to receive guaranteed settlements and enjoy the exact same tax deferral. If a recipient is called, such as the couple's kids, they come to be the recipient of an inherited annuity. Beneficiaries have multiple choices to take into consideration when picking how to get money from an acquired annuity.

{kind=link}

Table of Contents

Latest Posts

Analyzing Variable Vs Fixed Annuities A Comprehensive Guide to Fixed Annuity Or Variable Annuity Defining Retirement Income Fixed Vs Variable Annuity Advantages and Disadvantages of Different Retireme

Analyzing Pros And Cons Of Fixed Annuity And Variable Annuity A Closer Look at How Retirement Planning Works What Is Fixed Vs Variable Annuity Pros And Cons? Benefits of Tax Benefits Of Fixed Vs Varia

Exploring the Basics of Retirement Options A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Advantages and Disadvantages of Different Retirement Plans Why Tax Benefit

More

Latest Posts